This morning, Lisa, the HR manager of a manufacturing company that Keyman serves, sent this inquiry: “We have been providing healthcare benefits for our employees for the past 5 years through our HMO (Health Maintenance Organization) partner. The employees are using their coverage optimally based on the utilization reports. My question is, what other ways on how we can improve our healthcare and benefits program for our employees? We want to know if there are other benefits that we can consider to include this year.”

So, I called up the client and I found out that the reason why they want to enhance their benefit program is for them to be competitive and to help them attract and retain their best talents. Since I am familiar with their benefit program, I proposed the following enhancements:

1 – GROUP LIFE INSURANCE (GLI)

We can never emphasize enough the importance of having a good Group Life Insurance (GLI) in place. This provides coverage for the inevitable loss of life especially for an employee who is a bread-winner. As most financial advisors will propose, ideally one employee should be insured for at least the equivalent of 10-year’s worth of salary. However, due to budgetary constraints, most HR practitioners adapted the tiered benefit policy. In this setup, an employee with at least one year tenure is insured for an equivalent of 12-month’s worth of his salary. Those with 2 years tenure gets 24 months coverage and 36 months for those with 3 years. Most HR practitioners will put a cap for up to 36 months to minimize the costs. For example, an employee who has served for 1 year with a monthly salary of Php15,000 will be covered for Php180,000 worth of life insurance. And an employee with 3 years or more of service with say Php30,000 monthly salary will be covered for Php1,080,000.

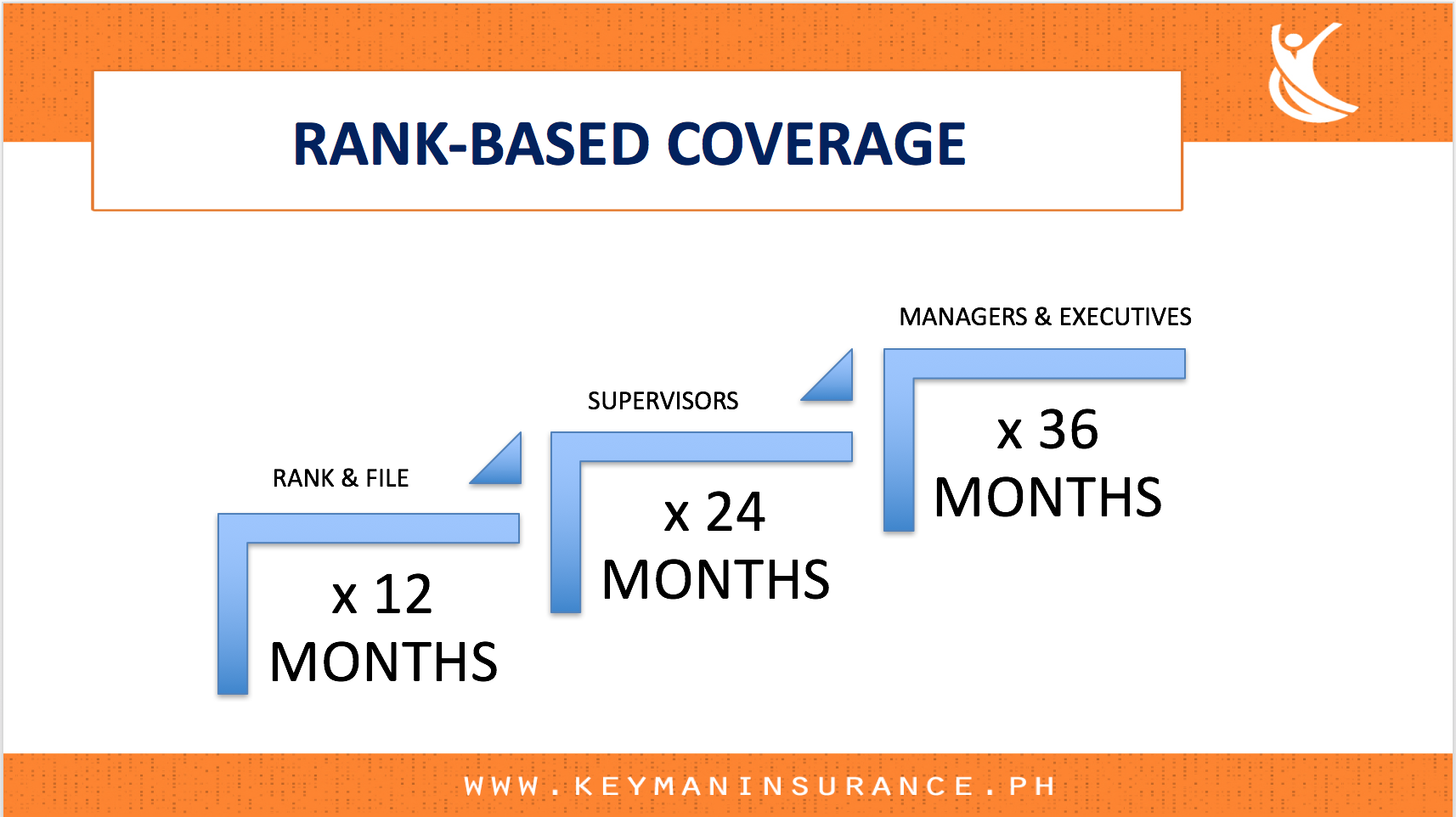

Another scheme is the Rank-Based Benefit Policy like the one below. The benefit coverage is based on the position level of the employee:

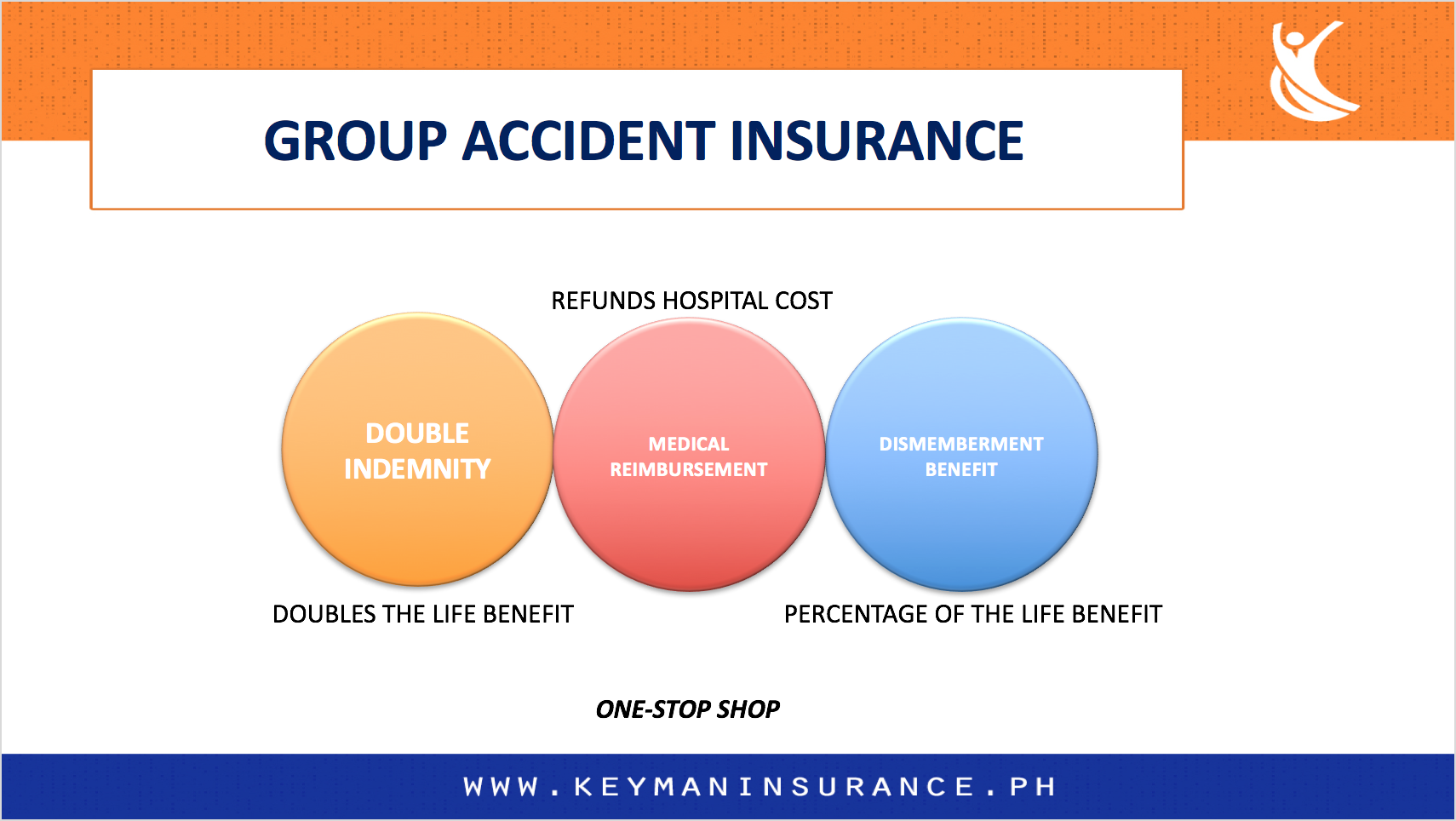

2 – GROUP PERSONAL ACCIDENT (GPA)

This is another benefit that is usually overlooked. GPA provides for a number of benefits: Dismemberment, Disability, and Medical Reimbursement. Why would you still need Medical Reimbursement when your HMO provides a full coverage and no cash-out plan? Because this comes in handy to cover outpatient medicines, un-coverable prosthetics, and metal implants usually encountered on accident claims. The Dismemberment cover provides for a cash benefit should any part of the body is removed, loss of hearing, or loss of eyesight among others.

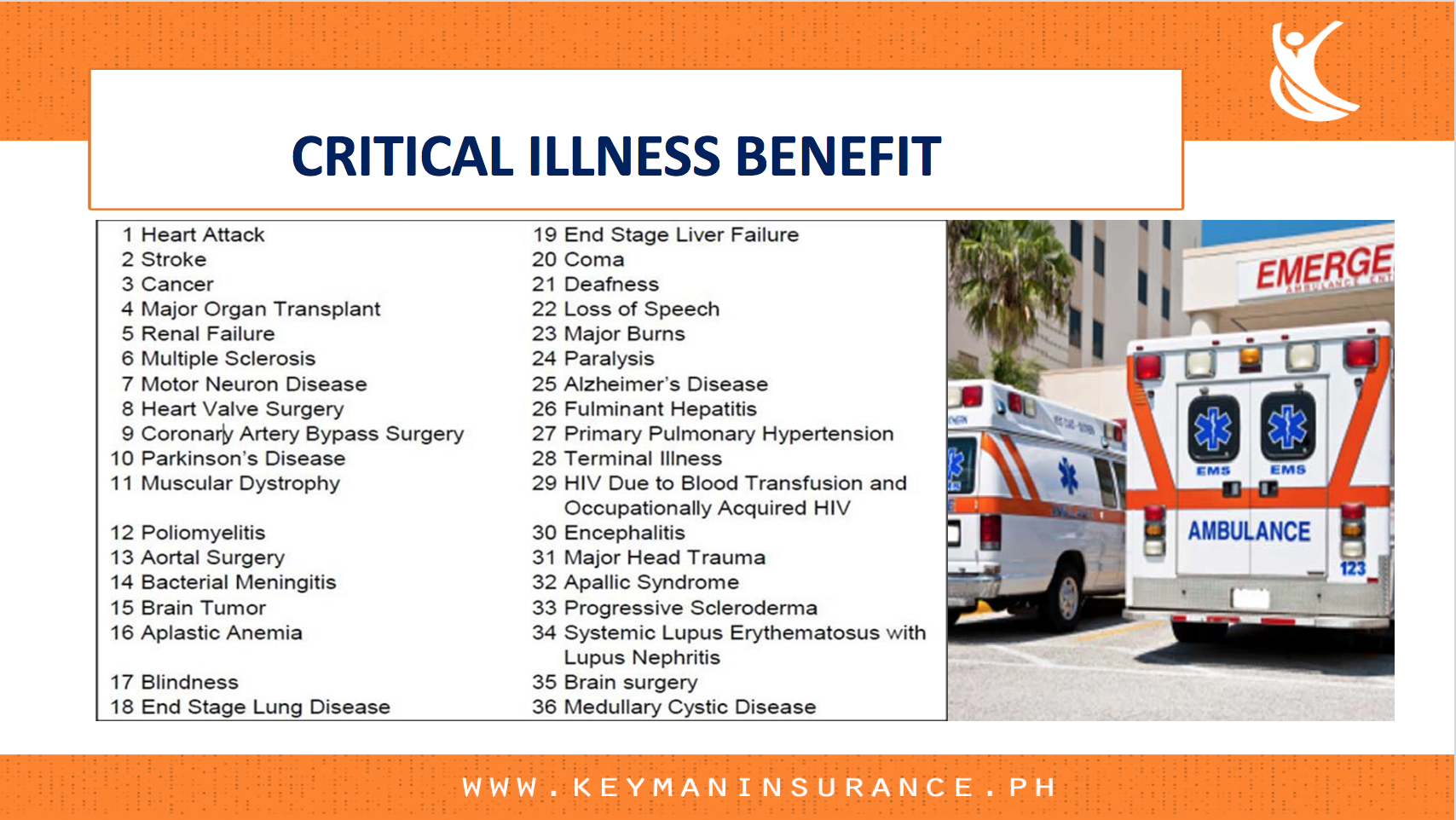

3 – CRITICAL ILLNESS BENEFIT (CIB)

It’s good that this client already has HMO. However, when a critical illness strikes like cancer, stroke, ruptured aneurysm, kidney failure, lung failure, and other similar cases, the maximum benefit limit (MBL) of the HMO program will not be enough. On the average, the MBL is only up to 100,000 per illness. If any of the conditions mentioned earlier will be experienced by the employees, their MBL will surely be maxed out and they need to shell out money from their savings or borrow from their relatives. Note that no lending institution will issue a loan for someone who is already on a critical condition. Good if we have this CIB so we can get our employees covered for as much as 1-2 million pesos.

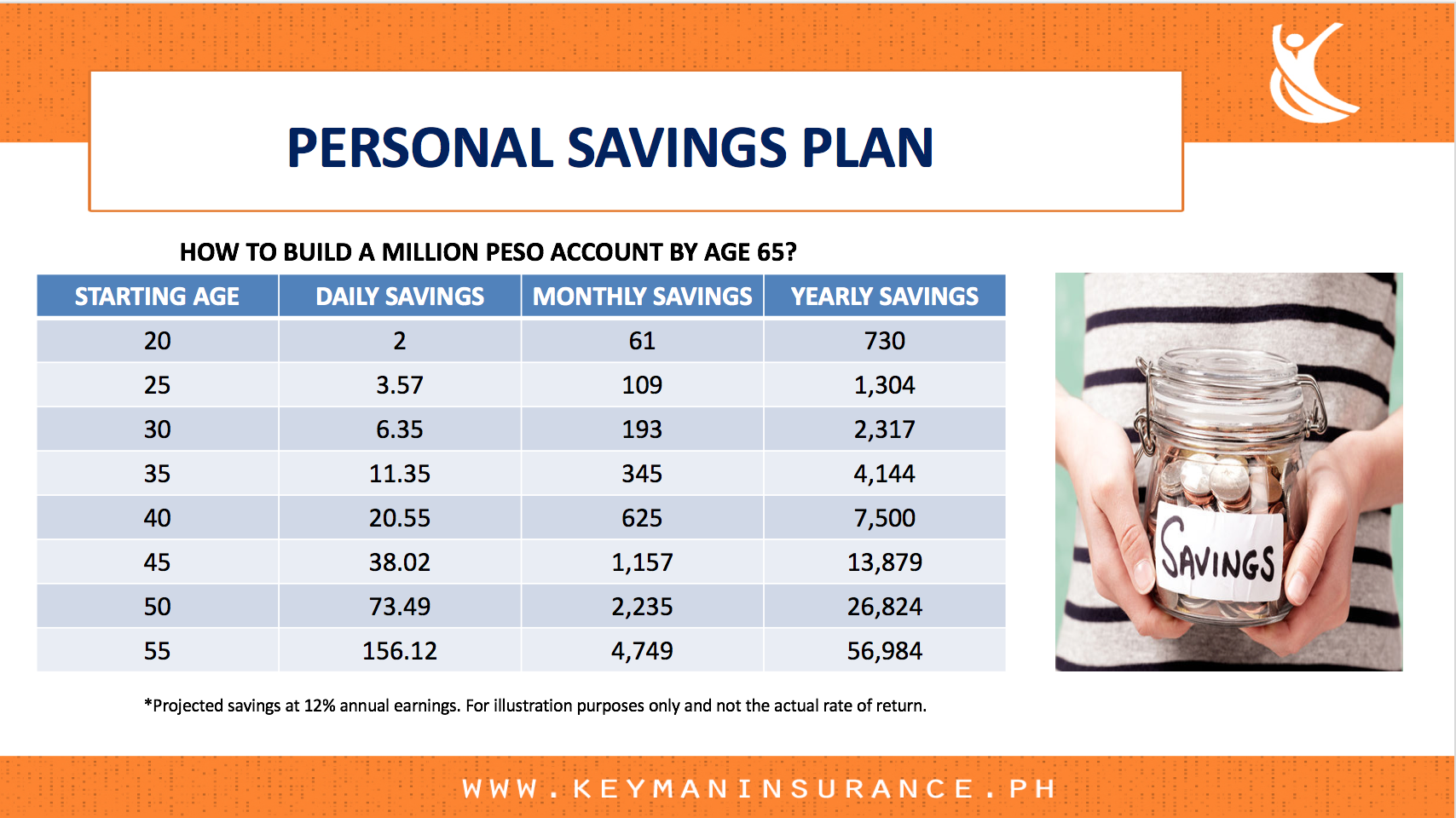

4 – PERSONAL SAVINGS PLAN

Most employees want to save for their future needs but are not well-informed on how to do it. So, they go for “paluwagan” system where together with their officemates, they put up a fund so that they can save for the rainy days. But since this is not a systematic and infallible scheme, it is prone to abuse and is designed to fail.

What we can do is to help educate the employees on the legally acceptable and effective savings plan. One that defines all the parameters and provisions in black and white. These parameters include the amount of monthly contribution, the projected amount of savings after a number of years, the amount of available emergency fund, etc. It also states the provisions on policy loans, fund withdrawals, and choice of investment fund.

Do you know that for a 25-year-old employee who continuously saves at least Php109 per month can accumulate up to Php1,000,000 by the time he/she retires at age 65? This can be achieved if the fund will have an annual rate of return (ROR) of at least 12% year after year. The ROR is not guaranteed since the fund is linked to the performance of the market or investment instrument chosen. But I hope you get the concept of accumulated savings. Regardless if the employee chooses a more conservative instrument like bonds and government securities, saving regularly over the course of time will prove to be beneficial in the end. As most financial gurus would advise, the only person who can take care of your older self is the younger self that you are today.

My recommendation for employees who are not really savvy in investing is to save on variable universal life or VUL. This life insurance product is linked to a chosen investment fund managed by the insurance company or its investment house. So, this product does not only provide protection on financial losses but also lets the policyholders grow their hard-earned money effortlessly.

5 – GROUP RETIREMENT PLAN

Drafting a retirement policy for the employees is provided for by Republic Act 7641 or also called the “Retirement Pay Law”. To put it simply, the minimum retirement benefit is computed as 22.5 days for every year of service. Some generous employers give more than what is required by law to be more competitive. We have clients who give as much as 150% of the current monthly salary for every year of service.

The minimum eligibility requirement is 5 years of service and the employee is already 60 years old. While the law prescribes the minimum requirement, it does not require the employer to set up fund in advance. The employer is only obliged to pay the retirement benefit to the employee as it becomes due.

However, for the employer to firm up its commitment with its employees, employers who set up a fund early on enjoys a high employee morale and confidence. Plus, the employer need not to shell out a huge amount all at once. They may start saving a portion of their excess funds to retirement instruments so they take advantage of fund accumulation. An excellently managed retirement fund can provide huge amount of savings for the employer.